Preliminary Durable Goods Orders:

June (Monday)

Durable goods orders grew modestly in June, but the pace of headline orders missed economists’ expectations.

- Expected/prior monthly change: +1.8%/–4.0%

- Actual change: +0.3%

Conference Board Consumer Confidence Index:

July (Tuesday)

Consumer confidence unexpectedly dropped last month because of worsening views of current economic conditions.

- Expected/prior month confidence: 92.4/92.2

- Actual confidence: 90.8

FOMC Rate Decision:

July (Wednesday)

The FOMC kept rates unchanged, largely meeting economists’ expectations. Three regional Fed presidents voted to raise rates.

- Expected/prior federal funds rate upper limit: 3.75%/3.75%

- Actual federal funds rate upper limit: 3.75%

Advance GDP Annualized:

Second Quarter (Thursday)

Economic growth slowed more than expected in the second quarter, with the annualized growth rate dropping to 1.5 percent, versus expectations for 2 percent.

- Expected/prior quarter GDP growth: +2.0%/+2.1%

- Actual GDP growth: +1.5%

Personal Income and Spending:

June (Thursday)

Personal income and spending rose less than expected in June after strong increases in May.

- Expected/prior month personal income change: +0.3%/+0.7%

- Actual personal income change: +0.2%

- Expected/prior month personal spending change: +0.4%/+0.9%

- Actual personal spending change: +0.3%

Equity

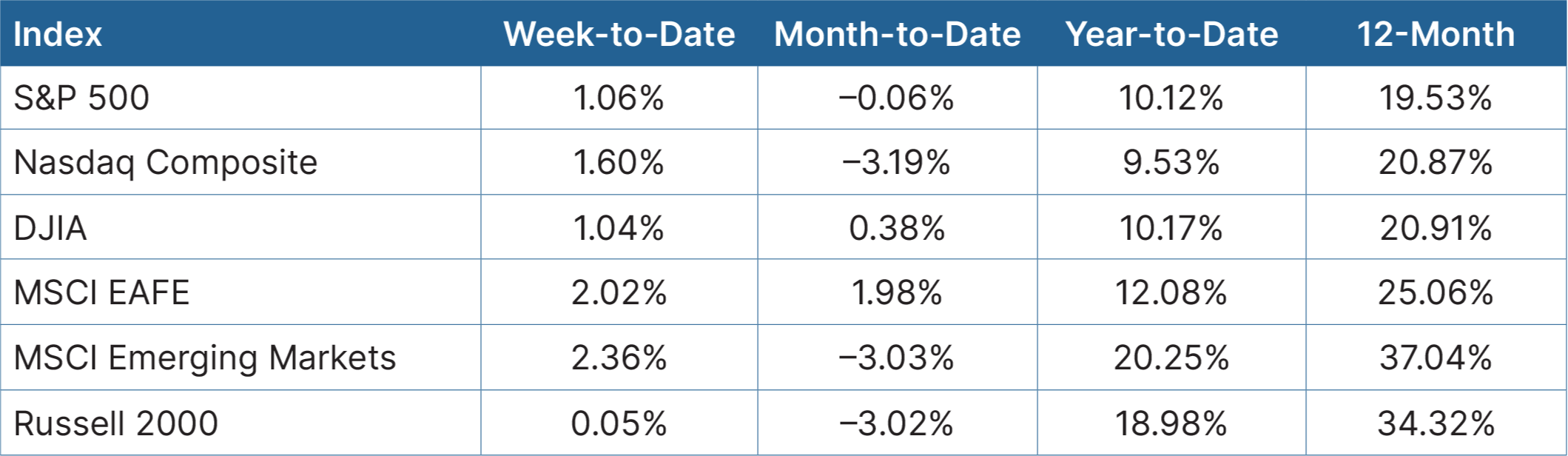

Strong late-week rallies helped markets close higher across the board. The Nasdaq Composite led the rally, rising 1.6 percent, while the S&P 500 and Dow Jones Industrial Average each rose 1 percent. With just two sectors driving the rally, market breadth was limited. The consumer discretionary sector increased more than 8 percent on the strength of Amazon, and communication services rallied more than 5 percent. Underperforming sectors included utilities and real estate, which declined 4 percent and 2 percent, respectively.

Source: Bloomberg, as of July 31, 2026

Source: Bloomberg, as of July 31, 2026

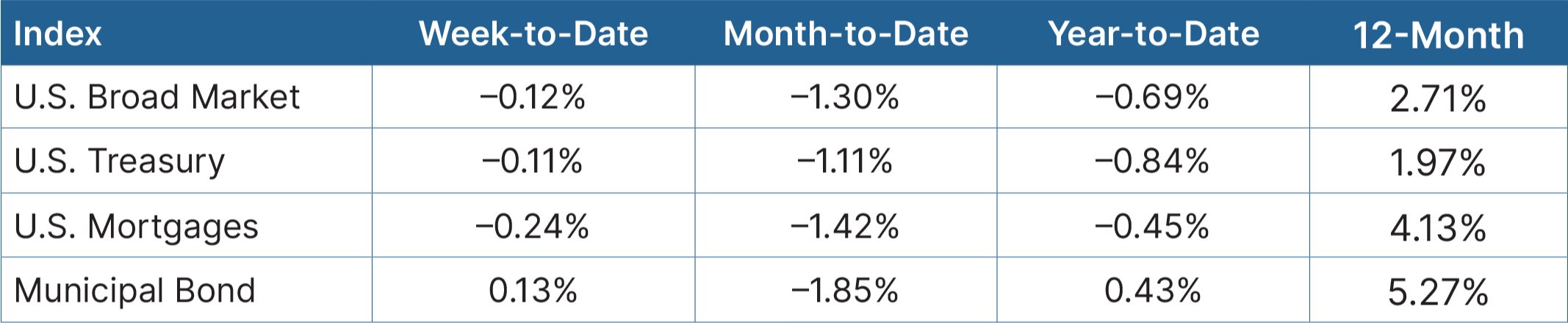

Fixed Income

The Treasury yield curve steepened after the Fed’s decision to hold rates steady, with the 2-year yield declining by 6 basis points (bps). The 30-year yield traded at its highest level in 19 years. Core bonds, Treasuries, and mortgages were down marginally; municipal markets moved up slightly.

Source: Bloomberg, as of July 31, 2026

Source: Bloomberg, as of July 31, 2026

Looking Ahead

Another busy week of economic reports will give investors insight into the strength of the manufacturing and services sectors. The highlight of the week will be the release of the July employment report on Friday.

- The week kicks off on Monday with the Institute for Supply Management (ISM) Manufacturing index for July. Manufacturing confidence is expected to rise after declining modestly in June.

- On Wednesday, we’ll see the ISM Services index for July. Confidence is expected to increase marginally. If estimates hold, the index will be in expansionary territory

- On Friday, we’ll receive the July employment report. Economists expect to see a modest 88,000 jobs created, which would be an improvement from June’s disappointing 57,000 jobs.

- It will be a busy week for earnings reports, with reports from Pfizer, Caterpillar, Disney, and Uber Technologies among the highlights.